Please consider some snips from the July 2012 ADP National Employment Report�

Employment in the U.S. nonfarm private business sector increased by 163,000 from June to July, on a seasonally adjusted basis. The estimated gain from May to June was revised down slightly,from the initial estimate of 176,000 to 172,000.Here are a couple of recent regional Fed manufacturing surveys to consider.

Employment in the private, service-providing sector expanded 148,000 in July after rising a revised 151,000 in June. The private, goods-producing sector added 15,000 jobs in July. Manufacturing employment rose 6,000 this month, following a revised increase of 9,000 in June.

Employment on large payrolls?those with 500 or more workers?increased 23,000 and employment on medium payrolls?those with 50 to 499 workers?rose 67,000 in July. Employment on small payrolls?those with up to 49 workers?rose 73,000 that same period. Of the 67,000 jobs created on medium- sized payrolls, 4,000 jobs were created by the goods-producing sector and 63,000 jobs were created by the service-providing sector.

Construction employment rose for the second consecutive month, adding 5,000 jobs. The financial services sector added 9,000 jobs from June to July, marking the twelfth consecutive monthly gain.

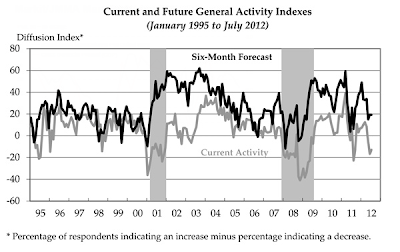

Philly Fed Manufacturing Survey

From the Philadelphia Fed Manufacturing Report ....

Indicators Suggest Continued DecreasesDallas Fed Manufacturing Survey

The survey?s broadest measure of manufacturing conditions, the diffusion index of current activity, increased from a reading of ?16.6 in June to ?12.9. This marks the third consecutive negative reading for the index (see Chart). Nearly 32 percent of the firms reported declines in activity this month, exceeding the 19 percent that reported increases. Indexes for new orders and shipments remained negative but increased 12 and 8 points, respectively.

Labor market conditions at the reporting firms deteriorated this month. The current employment index decreased 10 points, to ?8.4, its second negative reading in three months. The percent of firms reporting decreases in employment (18 percent) exceeded the percent reporting increases (10 percent). Firms also indicated fewer hours worked this month: The average workweek index increased 2 points but posted its fourth consecutive negative reading.

Here are a few snips from the Dallas Fed Manufacturing Survey.

Texas factory activity continued to increase in July, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, fell from 15.5 to 12, suggesting slightly slower output growth.US Services ISM and Factory Orders

Other measures of current manufacturing activity also indicated slower growth in July. The new orders index was positive for the second month in a row, although it moved down from 7.9 to 1.4. Similarly, the shipments index posted its second consecutive positive reading but edged down from 9.6 to 7.4. The capacity utilization index came in at 8.7 after rising to 13.3 last month.

Perceptions of broader economic conditions were mixed in July. The general business activity plummeted to -13.2 after climbing into positive territory in June. Nearly 30 percent of manufacturers noted a worsening in the level of business activity in July, pushing the index to its lowest reading in 10 months. The company outlook index remained positive for the third month in a row but fell from 5.5 to 1.6.

Labor market indicators reflected stronger labor demand. Employment growth continued in July, although the index edged down from 13.7 to 11.8. Twenty-one percent of firms reported hiring new workers, while 10 percent reported layoffs. The hours worked index was 4.1, up slightly from its June reading.

Price pressures were largely unchanged in July, although compensation costs rose at a faster pace. The raw materials price index held steady at 3, suggesting only slight increases in input costs this summer after strong upward pressure earlier in the year. Selling prices fell for the fifth consecutive month in July; the finished goods price index was -5.5, virtually unchanged from last month?s reading. The wages and benefits index rose nearly 10 points to 22.9, largely due to a marked rise in the share of firms noting increased compensation costs. Looking ahead, 36 percent of respondents anticipate further increases in raw materials prices over the next six months, while 25 percent expect higher finished goods prices.

Expectations regarding future business conditions were less optimistic in July. The index of future general business activity slipped from 1.3 to -7.3, registering its first negative reading in 10 months. The index of future company outlook remained positive but fell from its June level, coming in at 5.3. Indexes for future manufacturing activity also decreased, although all remained in strong positive territory.

On July 6th, I noted Services ISM Growth Slows - Jobs, Imports, Export Orders Contract.

Also on July 6th I noted Factory Orders Fall More Than Expected; Recovery Withers on the Vine

Given the global collapse in new orders including the US, weak ISM numbers in the US, and generally bad regional manufacturing reports, I believe there is potential for a really awful jobs report either this month or next and I will go for this month.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

No comments:

Post a Comment